Sustainability Advisory

We shape a more sustainable future through our environmental, social and governance advisory services for our clients' operations, products, and supply chain.

Our sustainability experts at Arcadis have compiled frequently asked questions about the Corporate Sustainability Reporting Directive (CSRD) to provide insights on what the new reporting guidance may mean for your company.

The Corporate Sustainability Reporting Directive (CSRD) is European legislation that came into effect on January 5, 2023. It requires companies to annually report transparently on their sustainability policies and performance. The directive replaces the existing Non-Financial Reporting Directive (NFRD) and significantly expands the number of companies covered, from 12,000 to 50,000.

The European Sustainability Reporting Standards (ESRS) determine the specific reporting requirements for each theme. These standards were published by the European Commission on December 22, 2023, and have been in effect since January 1, 2024. They enable better comparison and monitoring of European companies' sustainability performance.

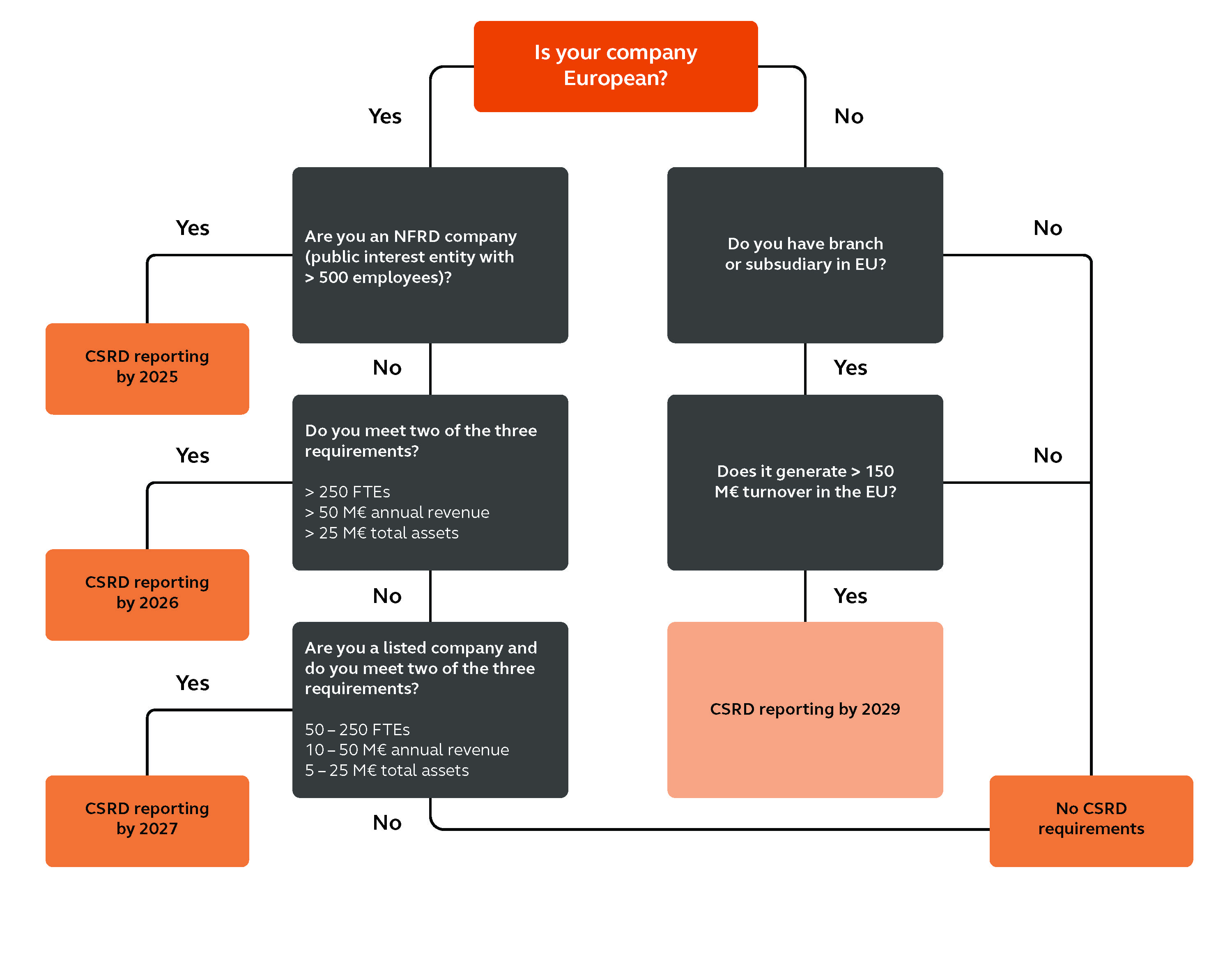

Many companies are still unsure if and when they have to comply with the CSRD. Here is an easy overview. Organizations that fail to comply or take appropriate actions run the risk of reputation damage, administrative, or financial sanctions.

Due to high inflation in recent years, the financial criteria for large enterprises and listed SMEs to be subject to CSRD have been increased by 25%.

Large enterprises must meet at least 2 of the following 3 criteria:

> 250 employees

> 50 million euros in turnover, and/or

> 25 million euros in total assets.

Listed SMEs must meet at least 2 of the following 3 criteria:

> 50-250 employees

> 10 – 50 million euros in turnover

> 5 – 25 million euros in total assets.

As a result of the increased criteria, certain companies may now fall into a different reporting cycle. However, please note that the proposed reporting timing remains unchanged for each group.

This timeline shows the year of reporting.

CLICK HERE

Starting from 2025, all companies that already fall under the Non-Financial Reporting Directive (NFRD) regulations must report on their sustainability performance for 2024. These companies meet at these two conditions:

Starting from January 2026, large European companies must also report on their sustainability performance for 2025. This includes companies that meet at least two of the following criteria:

Starting from January 2027, listed European SMEs join the list and must report on their sustainability performance for 2026. These are companies that meet at least two of the following criteria:

Starting from January 2029, non-European companies with at least one subsidiary or branch in Europe and a turnover of more than 150 million euros must report for the first time on the financial year 2028.

Additionally, a simplified reporting standard will be developed for listed SMEs and a voluntary reporting standard for non-listed SMEs. The first version of these standards is expected to be released in 2024.

This flowchart helps determine when your company must comply with the Corporate Sustainability Reporting Directive:

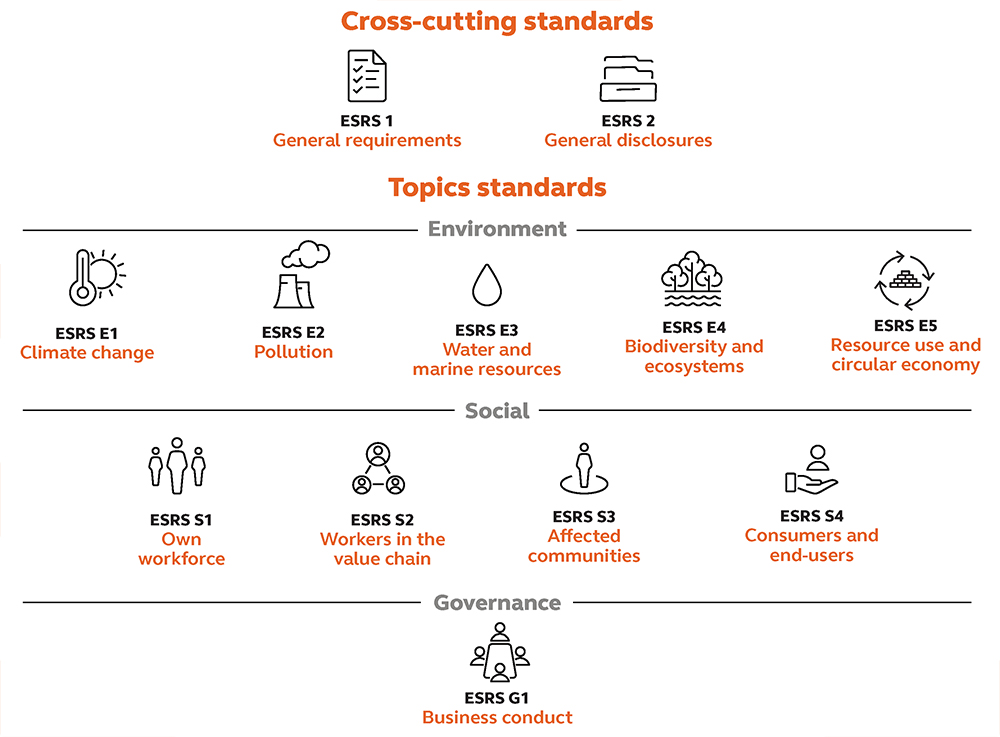

There are 12 European Sustainability Reporting Standards (ESRS) that determine the reporting requirements under the CSRD. These standards apply to all sectors and consist of two overarching or "cross-cutting" standards that apply to all themes.

In addition, there are 10 thematic or "topical" standards that cover different sustainability themes - Environment, Social, and Governance (ESG). Companies only need to report on the standards considered material or relevant in their materiality analysis.

Here is an overview of the 12 standards:

The sector-specific standards are expected to be released by mid-2026. These standards provide an overview of the impacts, risks, and opportunities that are likely to be material in a specific sector and are not adequately covered in thematic standards. The sectors in question are:

"Cross-cutting" standards

"Topical" standards

These address specific sustainability topics and are divided into themes and sub-themes. Thematic ESRS may include specific requirements that complement the general reporting requirements of ESRS 2.

ENVIRONMENT

To determine which sustainability themes are relevant for your company to report on, a double materiality analysis is conducted.

The European Sustainability Reporting Standards establish criteria to determine what is material. A company can set the threshold from which a theme ("topic") is considered material or relevant. A theme is considered material if it is material for at least one of the two (impact/financial).

Arcadis can guide you in conducting a materiality analysis. This is carried out together with a working group from the company. Stakeholders are also consulted to ensure that everyone's expectations and interests are considered in the materiality analysis.

The EU Taxonomy is a classification system with criteria that economic activities within certain sectors must meet to be considered sustainable. Its purpose is to inform investors and other stakeholders about the sustainability performance of companies in these sectors.

If your company falls under the scope of the CSRD, it is also required to report on Article 8 of the EU Taxonomy, following the same timing as the CSRD (see question 2). This means that you need to provide information on:

If your company does not fall under a sector included in the EU Taxonomy but is within the scope of the CSRD, you should report that your activities are non-eligible. More information to determine whether your company's activities are considered eligible can be found on the European Commission's website.

EU Taxonomy information should be included in your sustainability report. The ESRS contain links to the requirements of the EU Taxonomy, clarifying which information should be included in your sustainability report.

The first step is to determine which themes are a priority for your company through a materiality analysis. Then, it is important to compare your current management measures and reporting with the requirements of the CSRD. What has already been done? What is expected? What is still lacking? This outcome forms the basis for a step-by-step plan that establishes priorities for your company. Where action is still needed, clear objectives and KPIs are set for each theme. In the final step, you monitor the KPIs. Arcadis can guide you through all these steps and help you convert these intensive obligations into added value for your company.

Throughout our 135-year history, Arcadis has evolved into a company focused on fostering the transition to a more sustainable world. We do this through helping clients with sustainable strategies and offerings with a global presence, ensuring we meet local sustainability needs with an understanding of the market, and best practices from across the world. Learn more and connect with an Arcadis expert today.

We deliver sustainable design, engineering, and consultancy services for natural and built assets.